The landscape of American manufacturing is undergoing a historic structural transformation. Driven by supply chain vulnerabilities, acute skilled labor shortages, and aggressive federal legislation, domestic industrial companies are shifting capital expenditure (CapEx) away from simple brick-and-physical infrastructure toward deep, technology-driven automated machinery.

At the epicenter of this modern industrial revolution is automation equipment manufacturing. As industrial Original Equipment Manufacturers (OEMs) like Rockwell Automation, Emerson, and Honeywell scramble to meet the soaring demand for advanced factory systems, a secondary, highly critical bottleneck has emerged: the supply of custom, high-tolerance precision-machined components.

From programmable logic controller (PLC) aluminum housings and multi-axis servo motor mounts to pneumatic valve manifolds and heavy-duty conveyor wear tracks, factory automation is entirely built on physical, subtractive-machined metal and polymer parts. As a premier hub tracking global precision-manufacturing intelligence and industrial supply chain trends, 6CNC has synthesized the latest market data to analyze how this massive automation equipment buildout directly impacts downstream precision machining demand.

1. Macro Analysis: US Manufacturing CapEx Trends

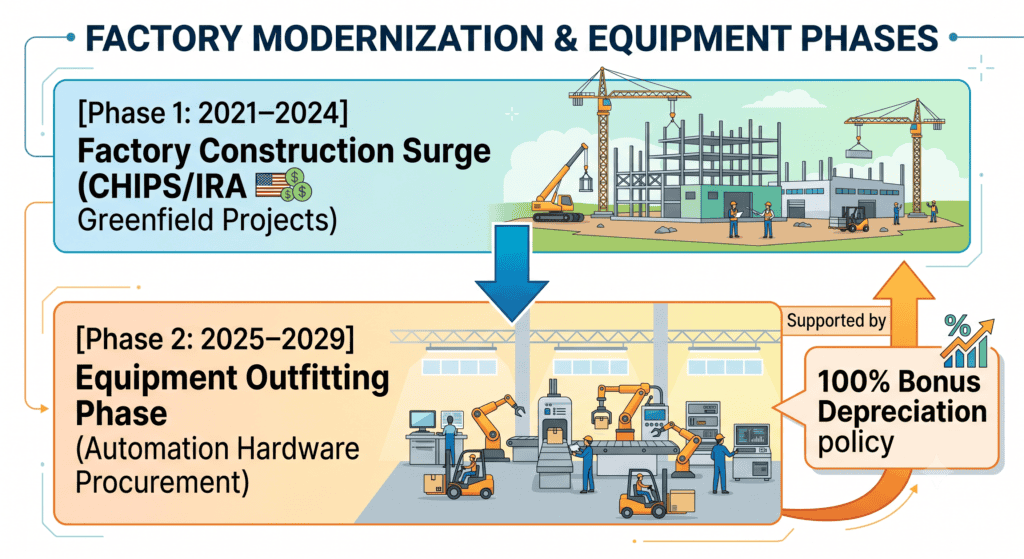

The trajectory of United States manufacturing investments has transitioned into a highly intensive “picks-and-shovels” phase. Following a multi-year surge in greenfield factory construction—spurred by the CHIPS and Science Act and the Inflation Reduction Act (IRA)—the physical structures are largely finalized. Capital is now flowing aggressively into equipping these shells with advanced, automated machinery.

Data from Bank of America Securities highlights that total US manufacturing CapEx reached $774 billion, representing a strong compound annual growth rate (CAGR) from pre-pandemic baselines. Crucially, while spending on factory buildings normalized, industrial equipment orders accelerated markedly.

[Phase 1: 2021–2024] Factory Construction Surge (CHIPS/IRA Greenfield Projects)

│

▼

[Phase 2: 2025–2029] Equipment Outfitting Phase (Automation Hardware Procurement)

▲ Supported by 100% Bonus Depreciation policy

This structural shift is heavily insulated by legislative tailwinds. The restoration of 100% bonus depreciation allows manufacturers to instantly deduct the full cost of automation systems and machinery, driving sustained, multi-year capital outlays. Furthermore, industry data shows that every $1 billion allocated to domestic high-tech manufacturing facility execution pulls through approximately $200 million to $300 million in dedicated automation spending.

2. The US Industrial Automation Market Size and Hardware Dominance

To accurately evaluate the down-funnel requirements for machined parts, the scope of “industrial automation” must be precisely defined. This category encompasses industrial control systems (ICS), distributed control systems (DCS), PLCs, human-machine interfaces (HMIs), motion control systems (servos, actuators, drives), and material handling/conveyor systems. It excludes standalone field robotics, which operate under a distinct capital cycle.

According to industrial market data from Mordor Intelligence and Ken Research, the United States factory automation and industrial controls market size is valued at $54.23 billion and is projected to expand to $88.05 billion by 2031, moving at a CAGR of 10.18%.

The Structural Reality: Hardware Rules the Floor

A common narrative among technology analysts is that industrial automation is primarily a software play, driven by Industrial IoT (IIoT), edge computing, and artificial intelligence. However, on the factory floor, software cannot function without a physical interface.

- Hardware Market Share: Physical hardware components command 71.25% of total automation market spending in the United States.

- Physical Shipments: Annual automation unit shipments in the US are expanding rapidly, on track to climb from 1.28 million units to over 2.15 million individual units annually by 2030.

This massive influx of physical shipments represents an unprecedented volume of enclosures, chassis, brackets, shafts, and fluid blocks that must be manufactured to commercial tolerances. To help procurement teams navigate these skyrocketing capacity constraints, the 6CNC digital manufacturing platform has systematically integrated domestic supply chains to streamline the sourcing of high-tolerance automation hardware components.

3. Quantifying Machined-Component Demand in Automation Hardware

Every single automated system shipped by an OEM or assembled by a tier-1 systems integrator relies heavily on a bill of materials (BOM) packed with CNC-machined parts. Subtractive manufacturing remains the non-negotiable choice for these components due to strict requirements for electromagnetic interference (EMI) shielding, structural rigidity, and heat dissipation.

The mechanical engineering breakdown of standard automation hardware reveals a high concentration of required CNC-machined features:

A. Industrial Control Systems, PLCs, and HMIs

Modern PLCs and industrial computers operate in harsh, debris-heavy, and high-vibration environment settings.

- Machined Profiles: Extrusions and casting clean-ups for heavy aluminum heatsinks, custom front panels, and specialized mounting bezels for capacitive glass screens.

- Tolerances: Flatness tolerances of $\pm0.02\text{mm}$ on heat-sink mating surfaces to prevent thermal runaway in high-density processing chips.

- Materials: Aluminum 6061-T6 (anodized for corrosion resistance), Stainless Steel 304 (for food processing environments requiring cleanability).

B. Motion Control: Servo Motors, Drives, and Actuators

Precision motion is the muscle of factory automation. The transformation of electrical energy into exact linear or rotary positioning requires high-tolerance mechanical housings.

- Machined Profiles: End-bells, splined rotor shafts, internal stator housings, gearboxes, worm gears, and specialized motor mounts.

- Tolerances: Extreme concentricity and runout tolerances down to $\pm0.005\text{mm}$ (0.0002 inches) to prevent harmonic imbalances, overheating, and bearing failure at high operating speeds (up to 10,000 RPM).

- Materials: High-tensile carbon steels (4140), Stainless Steel 416, and aircraft-grade aluminum.

C. Fluid Power and Pneumatic Automation

Automation networks rely on pneumatic actuators and vacuum grippers to handle physical components. Controlling this air pressure requires highly complex fluid channels.

- Machined Profiles: Multi-port pneumatic valve manifolds, valve spools, internal piston cylinders, and custom distribution blocks.

- Tolerances: Surface finishes of Ra 0.4 μm (16 micro-inch) or better on internal bores to maintain positive pressure seals and completely eliminate pressure drops across hundreds of thousands of cycles.

- Materials: Brass, Aluminum 6061-T6, and engineered plastics like Delrin (POM).

4. End-User Verticals Driving Automation Component Consumption

The demand for automation hardware—and consequently, precision parts machining—is distributed across several core domestic end-user markets. Each vertical introduces unique material and regulatory demands that shape local machining practices.

US Factory Automation Share by Core End-Market:

┌───────────────────────────────────────────────────────────┐

│ Automotive & Transportation (21.6%) │

├───────────────────────────────────────────────────────────┤

│ Food & Beverage (Fastest Growing - 12.75% CAGR) │

├───────────────────────────────────────────────────────────┤

│ Semiconductor & Electronics (CHIPS-driven) │

├───────────────────────────────────────────────────────────┐

│ Life Sciences, Pharma & Chemical │

└───────────────────────────────────────────────────────────┘

Automotive & Transportation (21.6% Revenue Share)

The ongoing reconfiguration of assembly lines to support electric vehicle (EV) battery pack assembly and modular power-train integration requires extensive tool changeovers. Machine shops catering to this sector produce massive volumes of heavy-duty fixtures, pneumatic manifold blocks, and custom linear actuator components to feed automotive tier-1 integrators.

Food & Beverage (Fastest Growing Segment: 12.75% CAGR)

Driven by strict sanitation regulations and a lack of floor labor, food and beverage plants are digitalizing rapidly. Because these environments are subject to intense chemical washdowns, standard aluminum and carbon steels are completely unusable. This segment creates an exceptional volume of work for high-end CNC machine shops capable of working with 316L Stainless Steel and medical-grade plastics, requiring smooth, crevice-free surface finishes to prevent bacterial contamination.

Semiconductor and Electronics Fabrication

As massive domestic semiconductor foundries enter operation, the demand for ultra-clean-room automation expands. Linear stages, wafer-handling gantry parts, and pneumatic vacuum modules require precision machining under strict contamination protocols, utilizing exotic materials like Teflon (PTFE), PEEK, and titanium.

5. Macro Data Matrix: Connecting Unit Growth to Machine-Shop Demand

To aid procurement managers, industrial analysts, and machine shop owners in calculating future addressable markets, the table below maps the projected physical volume growth of US factory automation hardware directly to its downstream impact on CNC machining operations.

| Automation Hardware Category | Projected US Market Share | Component Unit Volume Growth (2026–2031) | Primary Machining Geometry | Core Machining Material | Dominant Quality/Tolerance Metric |

| Industrial Control Systems, PLCs & HMIs | 40% to 45% | High (+8.5% YoY) | Prismatic enclosure panels, heatsink cooling fins, bezel pockets | Aluminum 6061-T6, Anodized Sheet Metal | Flatness and cosmetic finish (Ra 0.8 μm) |

| Motion Control Components (Servos, Actuators) | 25% to 30% | Very High (+11.2% YoY) | Cylindrical rotary shafts, deep-hole boring, external splines, internal threading | Alloy Steel 4140, Stainless 416 | Concentricity and Runout ($\le \pm0.005\text{mm}$) |

| Pneumatic & Hydraulic Manifolds | 15% to 18% | Moderate (+6.8% YoY) | Multi-axis cross-hole drilling, internal port geometry, O-ring groove cutting | Brass, Aluminum 6061, Delrin | Internal bore surface finish ($\le \text{Ra 0.4 }\mu\text{m}$) |

| Material Handling & Custom Conveyor Modules | 12% to 15% | High (+9.4% YoY) | Long-bed profile milling, heavy pocketing, large assembly drilling | A36 Structural Steel, UHMW-PE, Nylon | True Position accuracy over long lengths ($\pm0.1\text{mm}$) |

6. The Long-Term Outlook for Subtractive Machining

A critical operational metric for automation OEMs is the realized complexity per deployed automation unit, which is trending upward across the industry. Modern automation devices are denser, possess more integrated safety systems, and feature tougher mechanical configurations. For the precision machine shop, this translates directly to higher-value parts with more complex geometries, multi-axis setups, and tighter engineering requirements.

Furthermore, the fast-paced evolution of industrial technology means automation setups face rapid obsolescence cycles. Unlike historical legacy lines that stood unaltered for thirty years, modern automated lines require iterative tooling adjustments every 3 to 5 years. This continuous cycle of optimization ensures a steady, recurring stream of custom prototyping and low-to-medium-volume production runs for agile machining partners.

As American industry reinforces its infrastructure against global volatility, the relationship between the digital automation designer and the physical machine shop will tighten. Agile on-demand production networks, such as 6CNC’s precision CNC machining services, are rapidly transitioning from traditional backend vendors into the foundational infrastructure enabling the intelligent, automated factory floor.

![Comparison of Operating Principles: This figure illustrates a microscopic comparison of the surface waviness and residual scallop height generated by a face milling cutter and a ball-nose cutter under different stepover and step-down settings. [Figure 4-1]](https://6-cnc.com/wp-content/uploads/2026/06/image-2-300x199.png)